For many students in India, credit score, credit reporting, and credit history seem far away, a concern for working adults! However, students should be aware that in an age of digital and financial literacy the sooner you start earning and managing your credit, the more solid foundation you will have. Your credit score is more than just a number – it is you reputation to lenders, banks and for some jobs. Your credit score expresses your borrowing ability and whether or not you will pay back on time.

So what are some ways to build credit as a student without an income? Believe it or not, there are safe and simple ways to establish credit as a student while still a student.

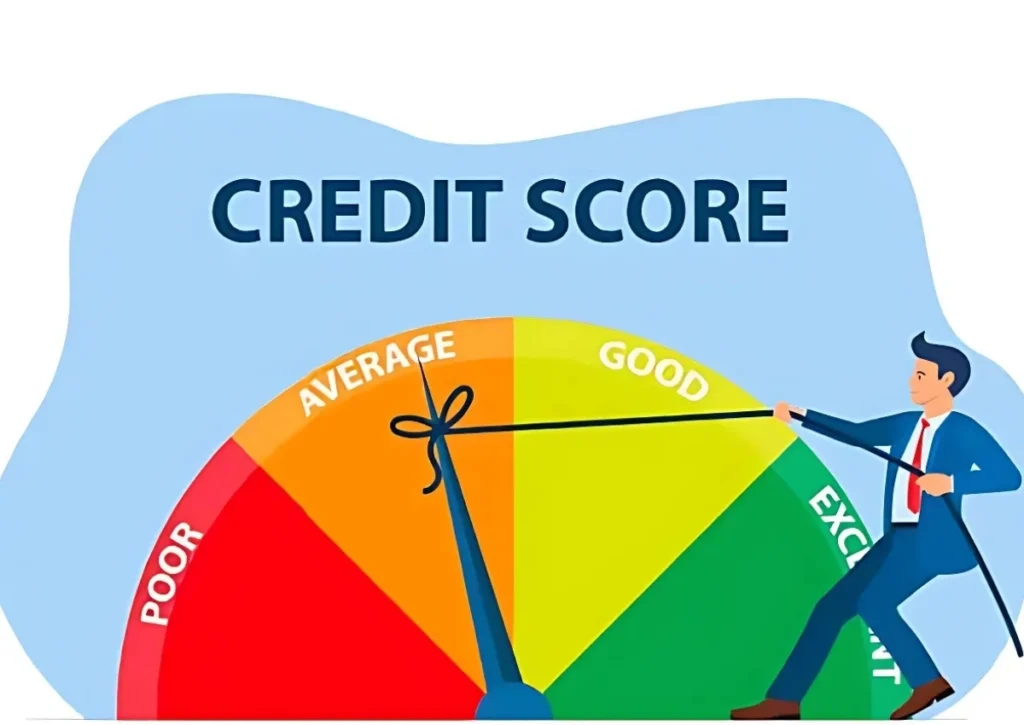

1. Understand the Basics: What is a Credit Score?

A financing mark may be a 3-digit quantity ranging from 300 to 900, granted by a debt agency such as CIBIL, Experian or, alternatively, by CRIF. That mark is planned on the basis of how you use credit, how much you borrow, how often you pay back, and how responsible you treat money. If your score is over 750, your chances of getting loans, credit card games, or even renting a house with ease increase.

But there’s a catch, you don’t get a debt mark unless you use credit. Therefore, in order to create a loan, you must have a couple of tasks to be reported to the aforementioned agency.

2. Start with a Student-Friendly Bank Account

Opening a student savings account with a reliable depositor is the first step towards building financial discipline. You can now benefit from this assistance.

Get into the habit of tracking spending.

Start a fixed deposit or savings goal.

Establish a relationship with a bank, which later helps in getting credit cards or loans.

The banks SBI, HDFC, Axis, and ICICI offer precise student transactions that do not require any documents and do not require any leverage.

3. Get a Secured Credit Card: Your Entry into Credit Building

As a student without income, getting a normal credit card can still be difficult. Nevertheless, yonder is a basic solution, a game of secured credit cards.These are published against a fixed deposit (usually 10,000 ). Typically, your financing limit is between 80 and 90 percent of your deposit. For the purpose of a demonstration.

If you make a ₹10,000 FD, your credit card limit will be ₹8,000 – ₹9,000.

You use the card normally – pay for food, travel, or books.

You repay the amount on time each month.

This project will be reported to the financing agency and will assist you in building a useful credit account free from all financial liability (as the lender already has your FD as security).

4. Make Timely Bill Payments – Every Rupee Counts

Many citizens believe that loan tons only include loans and debt card games. Despite this, your fiscal discipline is also demonstrated by the timely payment of regular bills.

As a student, you may be paying:

Mobile recharges or postpaid bills

Utility bills ( PG or hostel expences )

Subscriptions like Netflix, Spotify, Amazon Prime, etc.

A few stages, such as CRED, Paytm, and Bharat Billpay, allow users to report these payments to a loan agency. If you consistently pay above the era, you’ll build a record of reliable payments, even without traditional loans.

5. Become an Authorized User on a Parent’s Credit Card

If your ancestors, who are otherwise aged siblings, have a good credit story, you can ask them to add you as an authorized buyer of their plastic money. That is how it works.

You’ll receive a supplementary card with your name on it.

Their credit behavior (payments, utilization) will reflect partially on your profile.

Though it’s not always guaranteed, in many circumstances, it helps you develop a quick credit profile that does not have full accountability for refund. But it’s crucial that they handle their cards well because assuming they’ll default, they could hurt your reputation too much.

6. Use Credit Smartly: Spend Less Than You Can Repay

Once you’ve got plastic money, use it as a tool, not a license to spend too much. The aureate rule is.

Never spend more than 30% of your card limit.

Consequently, assuming your limit is 10,000, do not spend more than 3,000-4,000 a calendar month unless you are absolutely certain that you will receive a refund.

Paying the entire amount before the due date prevents interest charges and proves the lender that you are responsible. In the beginning, even a late payment can significantly damage your mark.

7. Monitor Your Credit Report: Know Where You Stand

Once a year, each agency (CIBIL, Experian, etc.) will provide you with a free credit report. ) on their official web site. This report shows that.

Your credit score

Your active credit accounts (if any)

Payment history

Any errors or fraud attempts

Keep an eye on this support your topographic point mistake and understand how your habit affects your mark. If you spot something wrong, escalate the dispute; it’s free and simple.

8. Try a ‘Buy Now, Pay Later’ (BNPL) App – Cautiously!!

Many financial technology software programs prefer LazyPay, Slice, or the Uni software that presents Buy, Pay afterwards ” assistance to students. The above-mentioned minicredit card game allows you to borrow small sums (500–5,000) and repay them after a couple of days or weeks.

This little loan, at a time when you’re paying right now, may contribute to your loan story. Although misuse may lead to a debt trap, therefore treat BNPL with the same sincerity as a credit card.

9. Avoid Loans Unless Absolutely Necessary

Study advances are fine if they’re needed, but do not take out special loans for unnecessary things like appliances or, alternatively, lifestyle expenditure. Unbarred progress is often reached with higher enthusiasm rates and stringent conditions for repayment.

As a student, it’s better to:

Borrow from family in emergencies.

Use a low-limit credit card for unexpected expenses.

Build a small emergency fund over time.

Unpaid loans or defaults can ruin your score for years.

Also check:- Mental Health Self-Care: A Complete Guide

10. Stay Consistent – Credit Building is a Marathon

It’s one of the biggest myths that your mark will increase in a couple of calendar months. The fact is, credit building takes time. It consists of roughly constructing adequate monetary transactions over periods.

Paying on time

Spending within limits

Avoiding too many credit applications

Keeping accounts active and positive

By the time you graduate, the above habit will give you a powerful credit mark, making it easier to get car loans, mortgages, or any other kind of better credit card game.

Structure lending as a student may seem like a mature task, but it’s actually one of the most intelligent things you can do at an early age. You need neither a salary nor a loan to get going; just a plan, some discipline, and an unchanging habit.

In a couple of years, when your friends are fighting over loan rejections or high interest EMIs, you will be grateful to have managed your financial journey during college.

Start small, stay consistent and let your credit profile grow with you.